{kind=link}

{kind=link}

"Credit card reward schemes

Credit card reward schemes are mostly a gimmick unless you're a big spender, since rewards cards nearly always charge hefty annual fees and high interest rates.

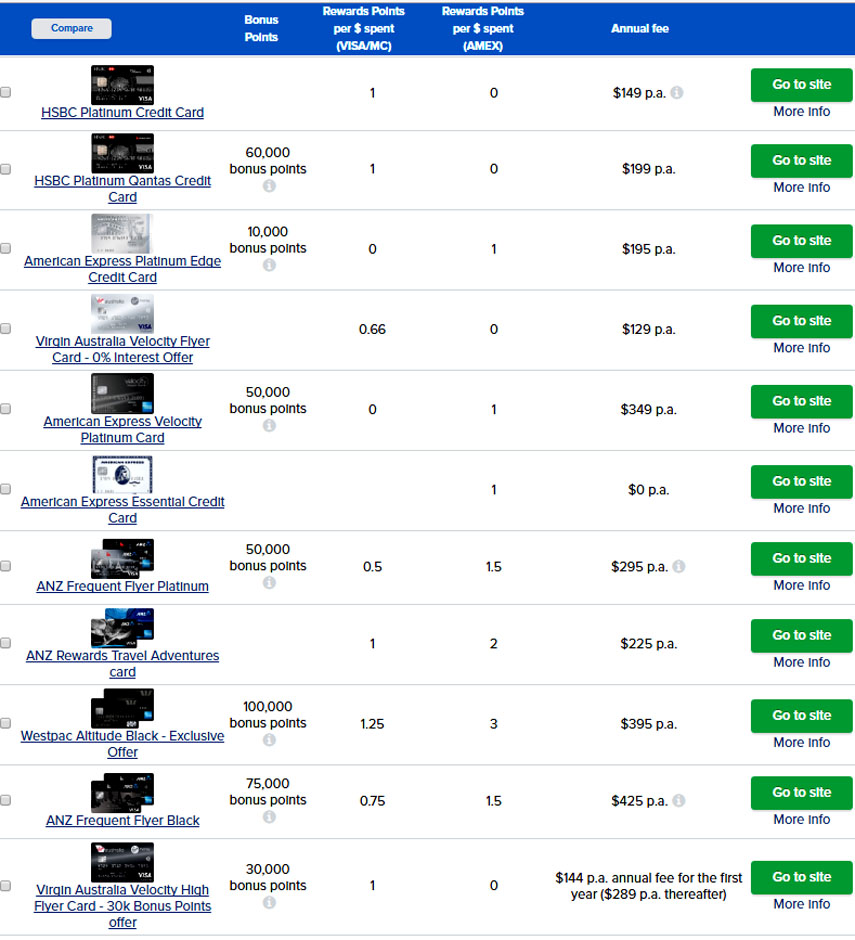

Credit card reward programs deliver little or nothing to consumers who don't spend generously via their credit cards.A CHOICE investigation of 63 rewards credit cards found that consumers would need to spend at least $2000 a month to get any return, while those who spent $1000 a month or less

would pay more in annual fees than they got back in rewards.Our research has also shown that cards that reward you with frequent flyer points are a far better deal than gift card or cash back rewards cards, where rewards accumulate at a much slower rate."

5. RBA's Review of Card Payments Regulation - Conclusions Paper - May 2016 - Section 3.4.8 Changes to benchmark compliance noted:

"When the benchmarks for credit card interchange fees were introduced in 2003, the Board’s aim was to limit the tendency for competition between schemes to drive up interchange fees. By setting the benchmarks in weighted average terms, the Bank allowed schemes significant flexibility to set different interchange fees for different transactions, some of which could be over the benchmark. Schemes have taken advantage of this, and of the current infrequent compliance arrangements, to develop commercial strategies that encourage issuers to maximise interchange revenue. The result has been that actual average interchange fees have tended to be higher than the regulatory benchmark and have drifted further above the benchmark between the three yearly compliance points. Accordingly, the benchmark has not represented an effective cap on average interchange fees."

6. Credit card reward value falls 63 per cent over past year - SMH - 1 Sept 2017 - John Collett